Consumer prices grew at the same pace in September as they had in August, a report released on Thursday showed. The data contained evidence that the path toward fully wrangling inflation remains a long and bumpy one.

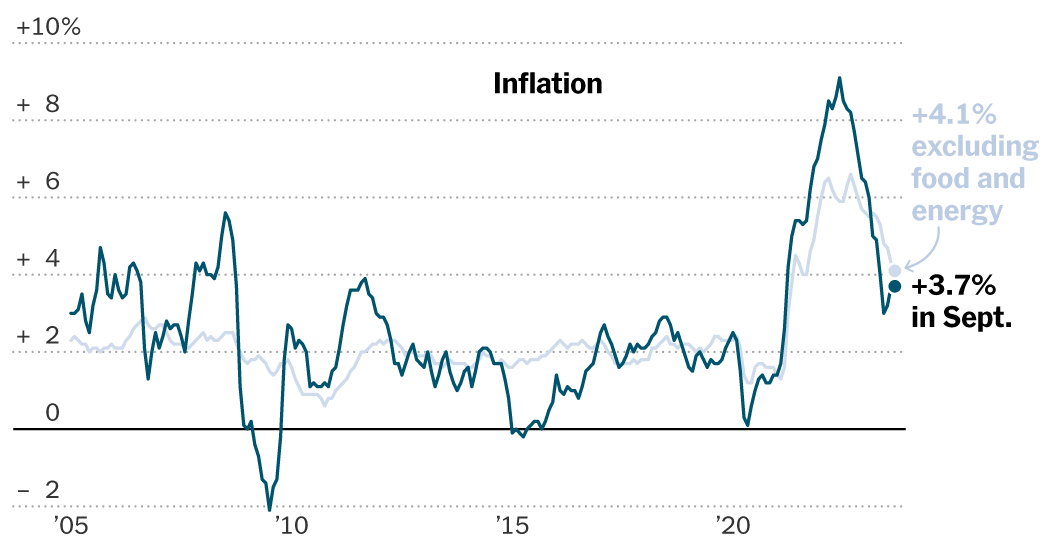

The Consumer Price Index climbed 3.7 percent from a year earlier. That matched the August reading, and it was slightly higher than the 3.6 percent that economists had predicted.

The report did have some optimistic details. After cutting out food and fuel prices, both of which jump around a lot, a “core” measure that tries to gauge underlying price trends climbed 4.1 percent, which matched what economists had expected and was down from 4.3 percent previously.

And inflation is still picking up at a much less rapid pace than in 2022 or even earlier this year. Even so, the fact that progress showed signs of stalling out is likely to keep officials at the Federal Reserve wary.

Fed officials have been raising interest rates since March 2022 in an effort to slow economic growth and wrestle inflation under control. They have already lifted borrowing costs to a range of 5.25 to 5.5 percent, up sharply from near-zero 19 months ago. Now, they are debating whether one final rate move is needed.

Given the fresh inflation data, economists predicted that policymakers are likely keep the door open to a final rate increase this year at a moment when inflation has begun to flag but is not yet clearly vanquished.

“This report still suggests that we have stepped out of the higher inflation regime,” said Laura Rosner-Warburton, a senior economist at MacroPolicy Perspectives. Still, “we’re not out of the woods — there are still some sticky corners of inflation.”

The report showed that prices declined for used cars and apparel. That added to evidence that healing supply chains were helping to lower goods prices and bring inflation down. At the same time, higher gas prices boosted inflation compared with a year earlier, as did a surprisingly strong pop in hotel prices.

Economists closely watch how much prices are increasing on a monthly basis to get a sense of how inflation trends are developing — and that part of the report offered some reasons for concern.

Price increases overall picked up by 0.4 percent in September from August, a quicker pace than policymakers would prefer but slower than 0.6 percent in the previous month.

But some of the factors driving that increase caught economists’ attention. Measures of housing costs climbed at a relatively quick pace after a recent slowdown. Fed officials and Wall Street forecasters have been expecting a steady slowdown in that measure because real-time rent trackers have been showing moderation for months.

Motor vehicle insurance is also continuing to climb quickly in price, and prices for recreation services — like sporting events — picked up sharply.

The pickup across a number of categories was enough to fuel concern that the marked slowdown in consumer price increases that occurred over the summer likely overstated progress.

“That summer of disinflation stuff was all about downside surprises,” said Omair Sharif, founder of Inflation Insights. “Now, there’s a lot of stuff that is surprising to the upside, and that’s probably the most concerning.”

The Fed is likely to take all of those changes into account as it thinks about the path ahead for interest rates. Central bankers have already lifted borrowing costs to a range of 5.25 to 5.5 percent, up from near-zero 19 months ago. Their next meeting will take place Oct. 31 through Nov. 1, and they are now debating whether they need to make one final quarter-point rate increase before leaving policy steady.

While investors widely expect Fed officials to leave interest rates unchanged in November, the odds of a December rate increase nudged up following the report.

Either way, Fed officials have been clear that they plan to leave rates set to a high level for some time, hoping that they will gradually trickle out through to economy, making it more expensive to borrow to buy a house or expand a business. That sustained restraint should help to cool demand, making it harder for companies to raise prices without losing customers.

So far, the economy has been surprisingly resilient in the face of higher borrowing costs. Consumer spending has remained solid, businesses continue to expand, and hiring was much stronger than economists had expected last month.

That has increased the chances that inflation could cool without a painful recession. At the same time, policymakers are keeping a close eye on the momentum, hoping that it will not give companies the confidence and wherewithal to keep raising prices at an unusually rapid clip.

At the same time, a recent move in market-based interest rates could help to cool the economy in the months ahead.

The Fed sets short-term interest rates, but the longer-term rates that matter most to consumers respond to both policy moves and other economic and financial factors. The yield on the 10-year Treasury bond has moved up sharply in recent weeks, which could help to cool growth even without additional Fed action.

Given those move, central bank officials have been clear that they will be patient as they consider future rate moves.

“We’re in this position where we kind of watch and see what happens,” Christopher J. Waller, a Fed governor, said during a public appearance on Wednesday. “The financial markets are tightening up, and they’re going to do some of the work for us.”

Mr. Waller said that the Fed is “keeping a very close eye on that,” and that officials would see “how these higher rates feed into what we’re going to do with policy in the coming months.”

Fed officials aim for 2 percent inflation over time, though they define that goal using a separate measure from the one released on Thursday. They prefer the Personal Consumption Expenditures index, which pulls from some of the same data, but which is calculated differently and released later in the month.

The P.C.E. inflation figures will be released on Oct. 27, just ahead of the Fed’s next meeting.